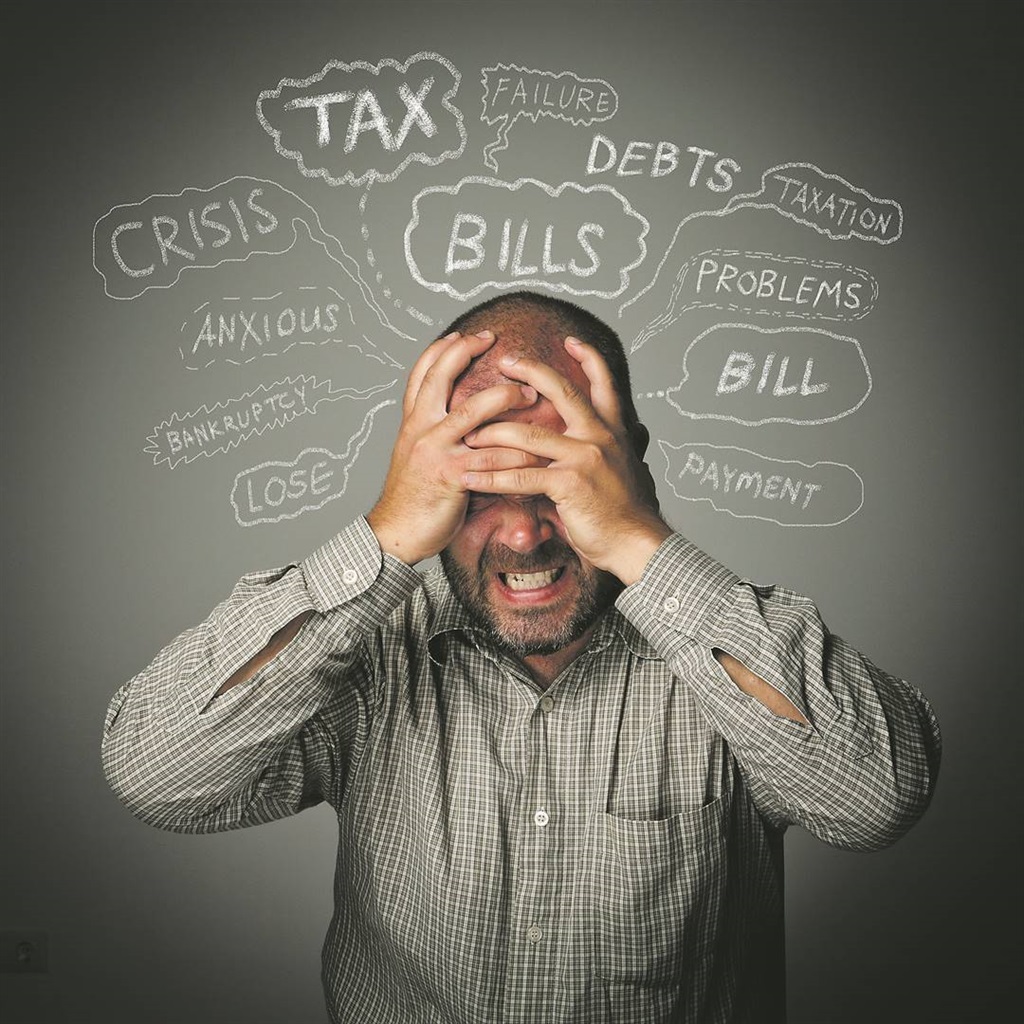

Several South Africans spend nearly 63% (two thirds) of their take-home wage paying off debt monthly. This is according to findings by debt counsellor DebtBusters.

This worrying revelation was the backdrop for Financial Awareness Day, observed on 14 August.

A range of reasons cited for several South Africans being trapped in debt include: the high interest and inflation rate, an increase in consumer prices, as well as hikes in electricity and fuel prices.

According to Statistics South Africa (Stats SA), consumer prices increased on average by 0,9% from June to July. Currently, South Africa’s interest rate is 8,25% while the inflation rate is 5,4%.

The price of fuel is now R23,70 per liter for 95 unleaded petrol in coastal regions, and R24,43 in the inland provinces. Diesel costs R19,82 per litre in coastal areas, and R20,53 per litre when bought inland.

Also, on 1 April, Eskom implemented a tariff hike of 18,65% for direct bulk electricity supply or non-municipal tariffs, while a municipal hike of 18,49% became effective on 1 July.

“Spending so much of your salary on debt is quite literally crippling. That is why they call it a ‘debt trap’,” said Stian de Witt, executive head of financial planning at NMG Benefits.

“And once you find yourself in a debt trap, it is very difficult to get yourself out of it.

“By making the necessary changes to eliminate debt, you will reduce your financial burden and ease your financial stress.”

He has advised affected people to seek help from a financial advisor to avoid being trapped in debt.

“Debt has a crippling effect on your emotional, physical, and mental well-being.

“It is critical to address the issue, ask for help, and get support by talking to a financial advisor,” he said.

A 2022 report by Genesis Analytics and the Financial Sector Conduct Authority (FSCA) revealed that more than half of South Africa’s credit-active consumers are over-indebted. The report stated that consumers largely spent borrowed money on financing necessities, with 43% spending the borrowed funds on food and 11% on clothing, bills, and monthly fees, respectively.

This trend is common among low-income individuals (earning less than R1 500 per month), grant recipients (approximately R1 500 per month), and individuals with informal jobs (more than R1 500, but less than R3 000).

“Being in debt is not a ‘game over’ scenario,” said De Witt, implying that hope can be kept alive.

“You can take back control of your financial well-being, and reduce your stress by implementing strategies and lifestyle changes, and seeking the necessary education and support.”